SVB - concern or FUD?

Introduction:

A lot of people are talking about ‘bank runs’, 2008 GFC, Lehman Brother comparisons etc due to the collapse of Silicon Valley Bank. Let’s delve into it - are we to be concerned or will this pass with time?

Who are SVB?

Silicon Valley Bank specialise in banking for tech startups by providing financing for almost half of US Venture-backed tech and health care companies.

What is the story?

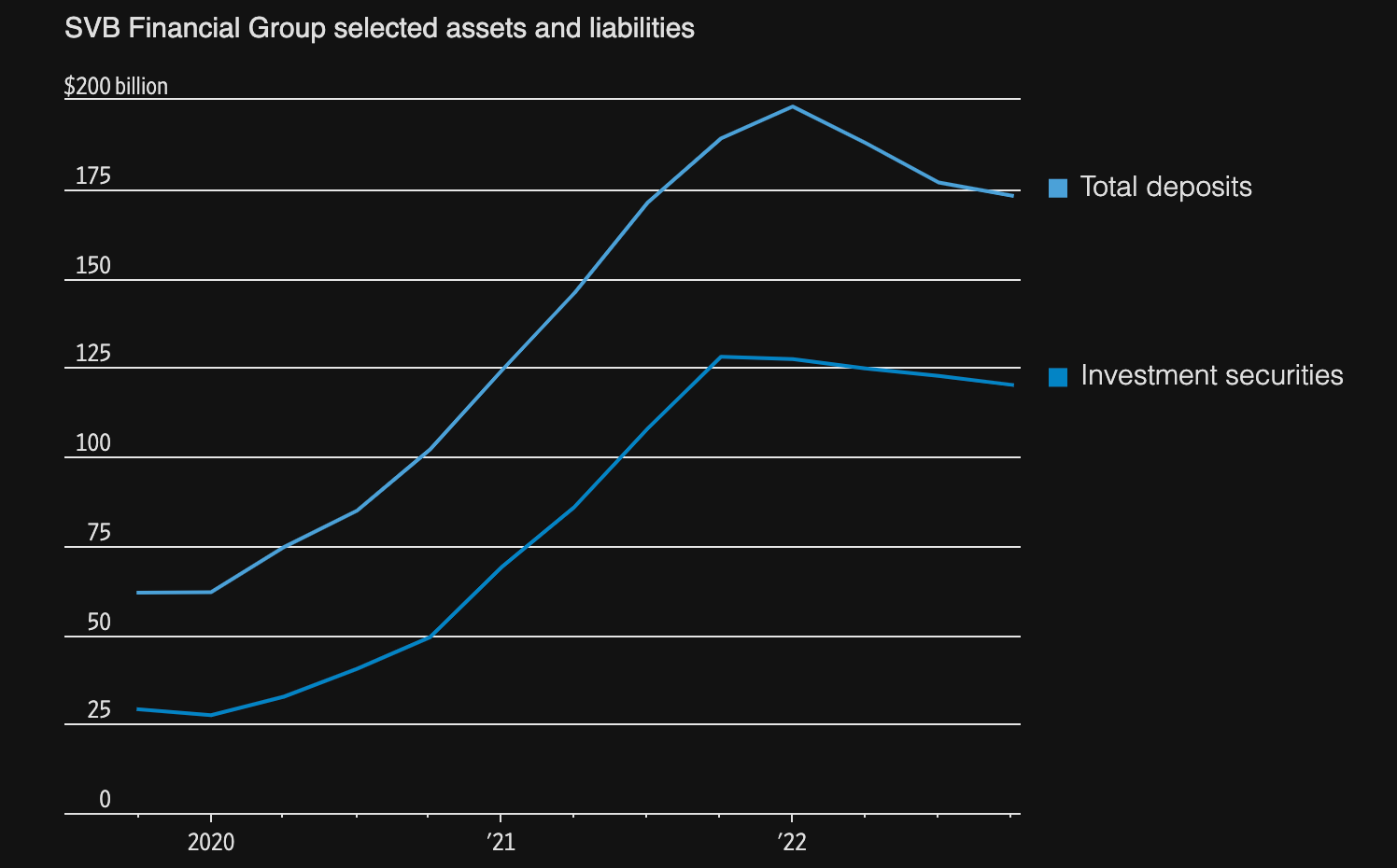

To understand the story, we must understand fractional reserve banking. So what’s this fractional reserve system about? Well, it’s how all of our economies operate. Essentially, it’s self-explanatory as a fraction of funds must be held in reserves. So your bank holds a % of your money, lending the rest of it out/investing the money to grow their total available funds. Usually, this is a great thing until ‘bank runs’ come into place which are depositors looking to withdraw their funds (2008 case study). In this case, SVB have had a surge of deposits:

Customers have recently tried to withdraw about $42bn of deposits, because its portfolio performance was so poor as interest rates were increasing, about a quarter of total deposits, but it couldn’t because the bank ran out of cash which led to this bank run.

In light of this, the FDIC (Federal Deposit Insurance Corporation) have took possession of SVB due to inadequate liquidity & insolvency according to the DFPI who appointed FDIC as the receivers. The FDIC insures deposits of up to $250k, but 90% of SVB’s depositors had a much more wealthier background as the deposits far exceeded above $250k with companies like Roku having almost $500M in the firm. So what happens now, do the depositors never see their money? well not exactly, FDIC grants a ‘receivership certificate’ to those who deposit over $250k which means that they get a short-term debt instrument issued by a receiver serving as a lien on the assets, so it provides funding to continue operations/protect assets in receivership.

So what’s next for the FDIC & what does it mean for the depositors?

The FDIC are currently looking to sell of its assets that SVB was holding onto which was a plethora of debt instruments eg MBS, Treasuries, Venture Debt etc. They’ll aim to do this by talking to banks like JPM, GS, MS etc & try to offload the assets - that’s if they can find buyers and if that doesn’t work, they’ll try to sell the whole bank, in which case a bailout may be in order. For depositors, funds are currently tied up but if the market is liquid & there’s buyers then it should all work out fine (even in the case of a bailout). Provided they’re not bailed out or able to sell their assets, and the company defaults then the depositors will face the music, but also key to understand that a lot of startup firms will suffer and jobs will be lost. However, there’s also too many pessimistic views here; many people think regional banks will be affected & this will be widespread like 2008 as it triggers fears, not so much in my opinion. I think the company will take on the loss & everyone will move on with their business, keeping funds in the same bank they’ve for their whole life.

What are the market implications?

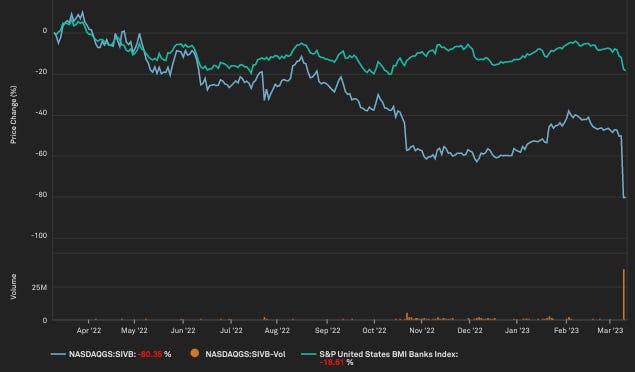

Bringing the banking sector down as the stock plummets

CDS skyrocketing

USDC depegging - because Circle, who issued USDC, revealed they had $3.3bn in SVB.

My thoughts:

Not much to worry about here, govt will either bail them out and all will be well or they’ll default and they’ll pay the price, & unemployment rate ticks a tad bit higher, but I don’t think the govt will let them default. I think comparisons to Lehman Brothers & 2008 are absurd. It’s important that most people remember these things happen & people move on for eg remember Credit Suisse, same thing happened - no one’s talking about it now.