Market March

Looking Back…

Review to last post: It seems SVB have been bailed out, although they’re not exactly framing it as such due to depositors being rescued excl creditors, employees, and shareholders.

What happened on the Monday Open?

huge sell-off in equities which resulted in DJIA & SPX being negative YTD

banking stocks trading being halted

unbelievable surge in VIX (20s to 30s in a day)

Market somehow included the likelihood of unchanged monetary policy, being priced in at 40%

Goldman expecting unchanged rate policy

50bps not being favourable (or even on the table) after story at SVB.

Introduction

In this post, we’ll go over my market bias & give reasoning for such. As always, we’ll also provide reasons why it may not work out as we forecast it to & see if there are any possible hedges for the situation, had it not turn out as bright as we desire. Before reading this post, I’d highly recommend you to get in tune with what my bias is & reasons for them:

The week ahead (GMT):

The Greenback

Markets are quite fickle as of recent - from pricing in 50bps to completely leaving it out within a matter of days. Rest assured, CPI will be the main contributor for FOMC to decide whether 50bp, 25bp, or 0bp is appropriate.

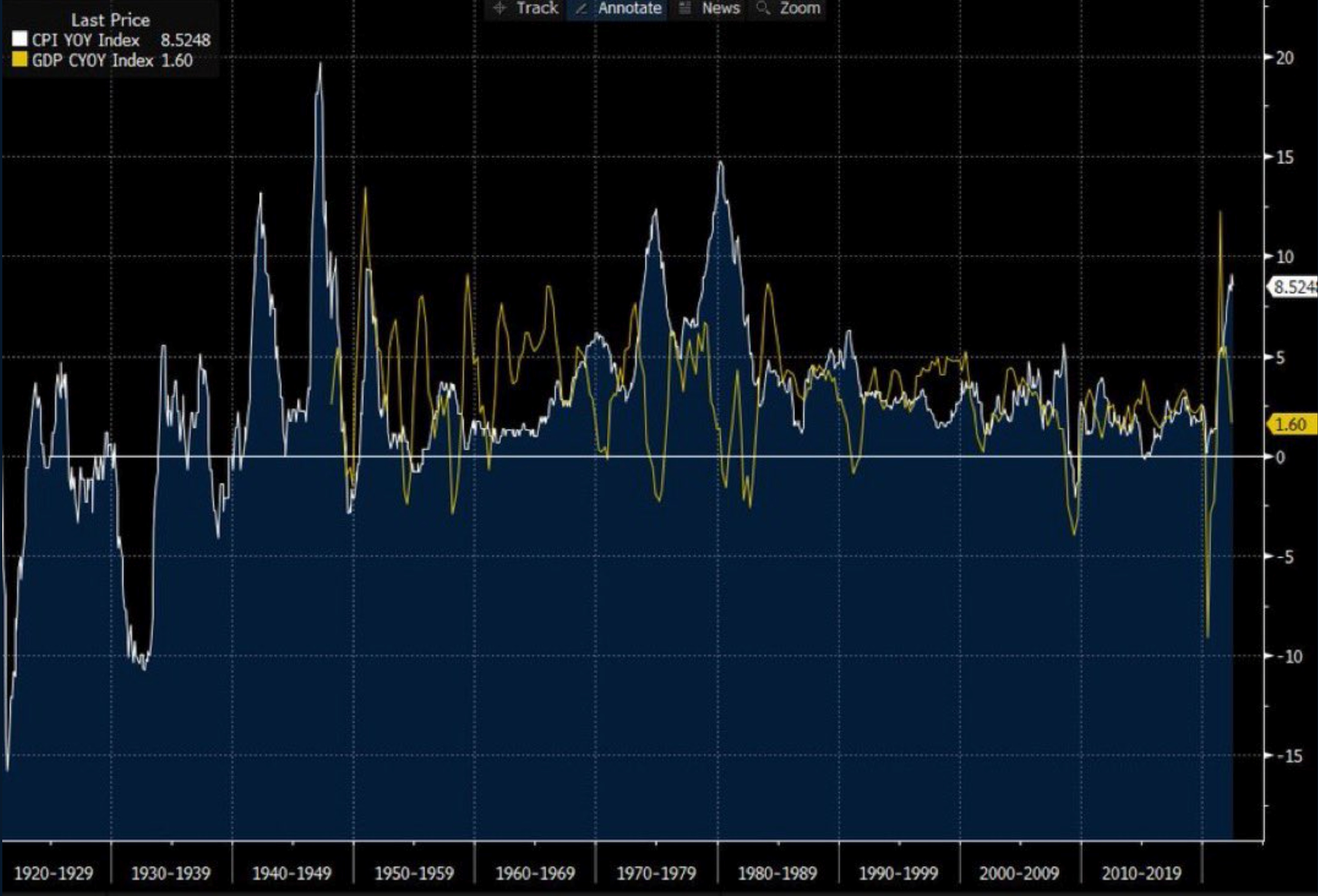

If you don’t understand CPI:

14/03/23 CPI outlook:

My personal view on inflation is that it’s quite sticky, we’re seeing that in the eurozone & it’s a matter of time before it comes to the US.

Analysts have beat down CPI with the market pricing in 6% vs a previous of 6.4%. The last print was a beat. This could be the beginning of a resurgence in inflation, as suggested by the recent PPI data, or it could show the last print as an anomaly. I expect the former.

≥ 6% = $ to surge, spx/dji/ndq selloff as more aggressive hiking becomes priced in. More hikes are good for the dollar because it makes it more attractive as an investment, which will have more inflows provided greater rates & ‘higher for longer’. More hikes are bad for equities because of the cost of lending etc; becomes harder to invest & make acquisitions, not pleasant circumstances.

< 5% = $ to plummet, spx/dji/ndq to rise as more dovish behaviour becomes priced in. Less hikes are bad for the dollar because it makes riskoff less attractive in comparison to riskon as less hikes are good for equities & makes it more desirable as an investment

Note: if you’re taking USD longs, the upside to that is astronomical vs shorts. Biden has himself publicly stated that he ‘feels good about the next print’ which has started to be priced in hence the rate hike probabilities. The whole market doesn’t believe in longing the USD, so the payoff is greater (not that you should trade it just because of better odds, it has to make sense).

I also believe the data for the following weeks will support more hikes from Powell, so my stance on the USD hasn’t changed - I’m merely just adding to my position. I will do this through shorting fibre (Eurodollar), and will set my SL to BE once above 20-30 pips to hedge my account against a < 5% CPI print.

Eurozone

Inflation beginning to slowdown (10.6% in Oct to 8.6% now), however the inflation is sticky. We’re seeing ups and downs, but more of a declining trend in inflation is being shown, and less rate hikes are supported by a weakening economic situation as PMIs (manufacturing) are considerably weak, employment chg suffering etc - seems something have broke in the economy, and its a call to pivot.

To take this trade on, I’m short EURGBP & EURCHF, the former will be explained in the next header but let me explain CHF. I like the swiss franc, and I’m very bullish on it as there was a CPI beat this week (+0.2%) leading to hawkish remarks from the SNB chairman.

The Great British Pound

Contrary to many, I’m bullish on the GBP as stated in my FX outlook issue. You can find the reasons why in there, but my trade has been proven to be right. We’ve seen GDP increase 0.3%, PMIs growing, NI trade deal etc - the economic situation is improving, and supports rate hikes. Inflation is still pretty bad, and we’ve not seen much of a decline in inflation.

However, the governor has unbelievably pointed to pausing rates at the current rate which astounded me, but they’ve to follow the data & it’s my view that they’ll see greater hikes are required. This means I’ll be extra cautious with GBP, setting SL more tightly, and eventually to BE, once comfortable to do so.

Kazuonomics

Due to the arrival of the new BoJ governor, I’m bullish on the JPY as I expect the YCC policy to be scrapped. I currently don’t have any positions for this open, but I’ll be actively looking for an opportunity. It may not be best to open USDJPY if you’re still bullish on USD. Seems more fitting for something like EURJPY.

Summary

Long USD

Short EUR

Long GBP

Long JPY

Outro

I wish you the best of luck within the next few weeks as markets are very turbulent. If you can share & like, it’d be much appreciated. Good luck!